Skip to content

Skip to content

European fintech is in the middle of a consolidation wave. In just the first half of 2025, there were 62 acquisitions, up from 57 in the same period last year. Now, one of the most talked-about deals is brewing: Dutch PSP Mollie is close to acquiring UK payments unicorn GoCardless.

At first glance, Mollie and GoCardless sound like a natural match. Mollie is one of Europe’s fastest-growing payment service providers, generating €214 million in revenue in 2024 (+28%) and finally turning EBITDA positive for the first time since 2018. GoCardless, founded in 2011, has meanwhile established itself as a leader in recurring payments and open banking, processing an impressive £39.6 billion in transactions in FY2024.

But there’s a twist. For all its scale, GoCardless is still loss-making. The company reported £126.8 million in revenue (+38%) but also a net loss of £35.1 million (a 55% improvement from the previous year) and a pre-tax loss of £34.5 million. To tighten its operations, it has already made difficult moves, cutting staff by 20% and shifting some activities to Eastern Europe. Profitability, according to management, won’t arrive until the end of 2025.

Still, GoCardless is not just another loss-making fintech. What it brings to the table is scale, momentum, and a set of capabilities that Mollie doesn’t yet have. Mollie’s strength lies in online and card payments for SMEs, while GoCardless specializes in recurring payments and direct debits. Put together, they could offer a more complete ecosystem, cards, bank-to-bank, and open banking under one roof.

The turnaround story also makes the deal more compelling. GoCardless has already halved its losses and is on a clear trajectory toward profitability within 18 months. When combined with Mollie’s already-profitable platform, the result could be a much stronger financial position than GoCardless could achieve alone. And then there’s the question of scale. Combining Mollie’s €214 million with GoCardless’ £127 million in revenue creates a company with over €335 million in annual revenue and nearly £50 billion in processing volume. In other words, Mollie could spend years building its own direct debit rails, or it could acquire Europe’s category leader overnight.

What happens to the workforce after an acquisition?

So far, the headlines have been about revenue, growth, and profitability. But the real story in any acquisition lies with the people. What happens to the workforce once two companies decide to come together? At this stage, Mollie and GoCardless haven’t announced their post-acquisition strategy, which means we can only work with scenarios. And typically, there are two extremes, and one middle ground, that shape how the workforce will be impacted.

Scenario 1: Full integration (The merger model)

In this version, GoCardless is fully absorbed into Mollie. The brand disappears, the systems are merged, and employees are consolidated into one single organization. The upside is obvious. A unified brand strengthens market positioning and makes it clear for merchants who they’re dealing with. The combined product offering, Mollie’s card and e-commerce platform alongside GoCardless’ direct debit and open banking rails, becomes a real rival to Stripe or Adyen. Shared infrastructure, compliance, sales, and support cut costs, while the merged merchant base produces richer data for insights and cross-selling.

But the risks are also clear. Integrating two different tech stacks, compliance processes, and product roadmaps is a messy business. Cultural misalignment is another hurdle: Mollie has grown as a fast-scaling, product-driven Dutch fintech, while GoCardless is a UK-based, API-first company with a B2B focus. For employees, this could mean morale issues, duplicated roles, and in some cases, redundancy. Even for customers, a forced migration to one system can cause outages, dissatisfaction, and ultimately churn. And let’s not forget: GoCardless’ brand equity is valuable, removing it could unsettle its loyal customer base.

Scenario 2: Stand-alone subsidiary (The loose acquisition)

Here, Mollie buys GoCardless but lets it continue operating independently under its own brand, with the quiet add-on: “a Mollie company.” This approach preserves what GoCardless is best known for, recurring billing and open banking, while reducing the immediate risks of system integration. Customers would notice little change, and both companies could continue innovating in their respective niches.

But keeping everything separate comes at a cost. Two organizations mean duplicated functions in sales, HR, finance, and compliance. Running them in parallel can be expensive. There’s also the risk of “strategic drift”: without close alignment, Mollie and GoCardless could build overlapping products, wasting resources.

Scenario 3: Hybrid integration (The middle ground)

The third path is somewhere in between. Mollie could integrate the back-end systems, compliance, risk, and infrastructure, while keeping GoCardless alive as a brand and product line.

This model offers the best of both worlds. The companies capture cost savings where it matters, while still protecting GoCardless’ trusted identity in recurring payments. Merchants benefit from cross-selling opportunities: Mollie customers gain access to direct debit and open banking, while GoCardless users get card and e-commerce capabilities. Having two strong brands under one umbrella also diversifies risk and provides flexibility, if one brand weakens, the other can take the lead.

Still, hybrid integration isn’t free of challenges. Aligning IT systems and compliance processes across two brands is complex. Positioning can get confusing for customers, do they sign with Mollie, or with GoCardless? And because not all duplication is removed, the full cost savings of consolidation aren’t captured.

The workforce behind the headlines

When two fintechs come together, the numbers everyone watches first are revenue and losses. But another set of numbers often says more about the future: the workforce.

Growth trends

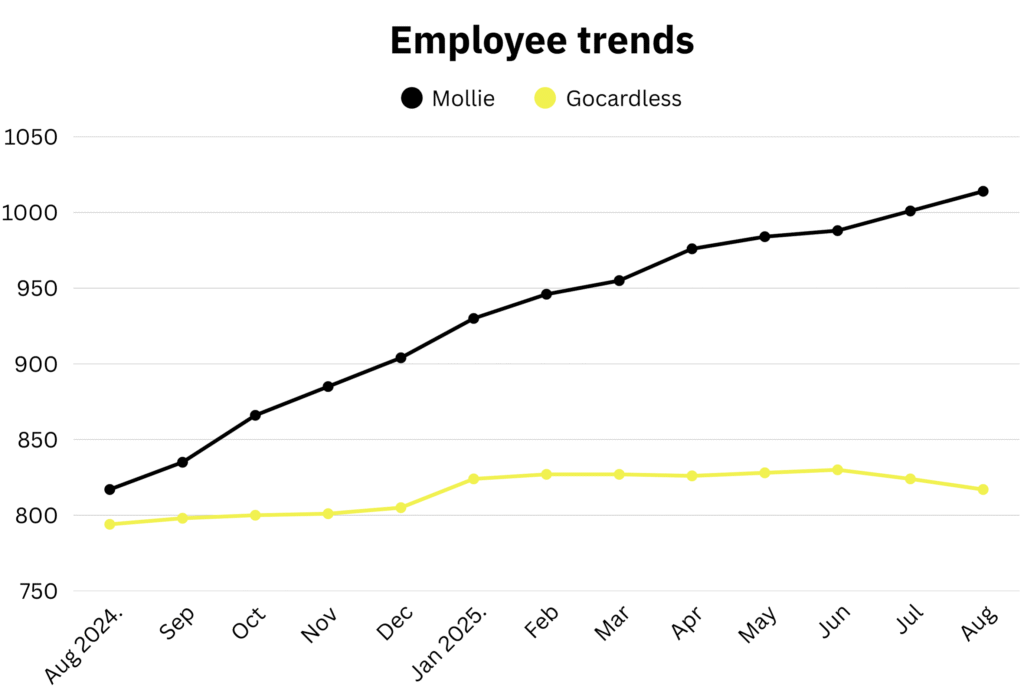

Over the past year, Mollie’s headcount has been on a steady upward climb, passing the 1,000 mark in August 2025. This growth reflects its international expansion and its product-first strategy, scaling its engineering base to support new features and markets.

GoCardless, by contrast, has kept its headcount relatively flat, hovering in the low 800s. After earlier workforce cuts, it’s been in a period of stabilization rather than expansion. In other words, Mollie is in growth mode, while GoCardless is in efficiency mode. Bringing these two trajectories together would mean blending a scaling company with one that has recently been focused on discipline and control.

Geography

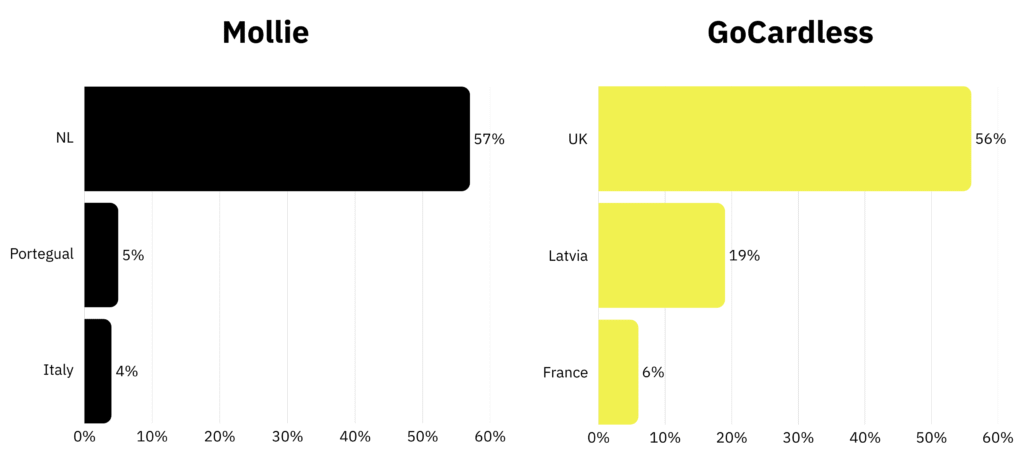

Mollie’s workforce is concentrated: more than half of its employees are in the Netherlands, with only small hubs in Portugal and Italy. This reflects its DNA as a Dutch fintech with strong home-market roots.

GoCardless is more geographically distributed. While a majority of its team is in the UK, it also has a sizeable hub in Latvia and a smaller but notable presence in France. This spread shows how GoCardless has leaned on regional hubs to manage costs and scale its customer operations.

If you compare the two, Mollie looks like a centralized product shop, while GoCardless looks like a networked organization with operational hubs in different countries. Combined, they’d have complementary footprints, Mollie dominating in the Benelux, GoCardless strong in the UK, with an efficiency hub in Eastern Europe.

Roles and functions

Inside the organizations, the split of roles also tells an interesting story.

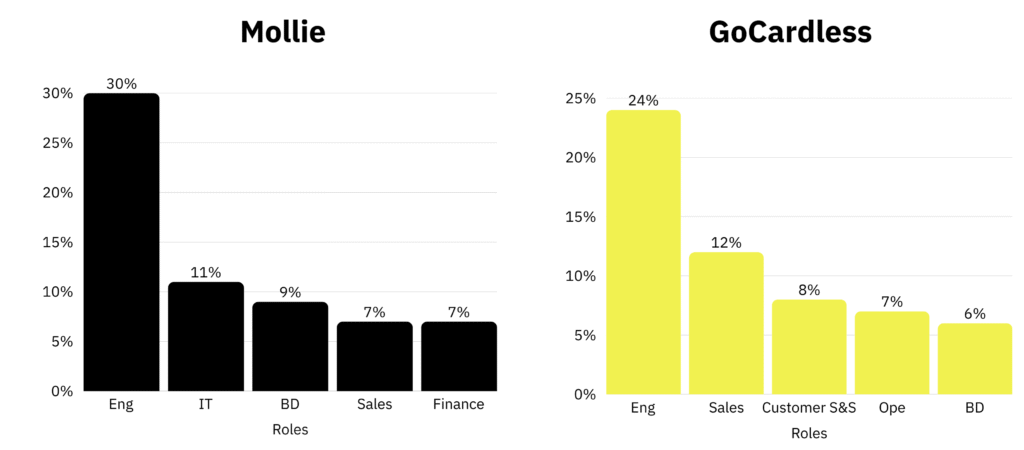

Mollie’s workforce is heavily weighted toward engineering (about one in three employees), with IT and business development following behind. Sales and finance make up a much smaller slice. This is the classic structure of a product-led fintech: build first, sell second.

GoCardless, on the other hand, has a more balanced structure. Engineering is still the largest single group, but the company invests much more in sales, customer success, and operations. That’s a reflection of its recurring payments model, where customer support and billing operations are as critical as the technology itself. Together, these profiles highlight a key difference. Mollie’s strength is in building sleek, scalable products. GoCardless’ strength is in running and supporting a payments network at volume.

Tenure and attrition

Another important layer is employee tenure and attrition.

GoCardless’ workforce has slightly longer tenure, an average of 2.7 years versus Mollie’s 2. That extra experience can be a stabilizing factor during change. But both companies face relatively high attrition rates (around 19–20%), meaning one in five employees turns over each year. Add the uncertainty of an acquisition, and retention becomes a critical risk.

Put all of this together, and you see two very different workforce profiles:

- Mollie: centralized, engineering-heavy, scaling fast.

- GoCardless: distributed, customer-facing, stabilizing after cuts.

If they do come together, the challenge won’t just be integrating technology or balancing profit and loss. It will be about aligning these two workforce models, one sprinting ahead, the other pacing itself, without losing the strengths that make each valuable.

Talent mapping & workforce planning advisory for Mollie + GoCardless

No matter which integration path Mollie chooses, the workforce will ultimately decide whether this acquisition succeeds or fails. This isn’t just about combining headcounts, it’s about mapping out where overlaps exist, where complementary strengths lie, and how people can be redeployed and reskilled to build something bigger than the sum of its parts.

1. Talent mapping – Identifying overlaps and gaps

The combined company would bring together nearly 500 engineers. At first glance, this might look like duplication, but in reality the two groups are complementary. Mollie’s engineers are primarily focused on card and e-commerce infrastructure, while GoCardless’ talent base is steeped in account-to-account and open banking. Rather than consolidating these roles, the smarter move would be cross-training: letting GoCardless engineers strengthen Mollie’s A2A product line, while Mollie’s teams help scale GoCardless’ SME integrations.

The sales and business development functions show a similar story. Together they make up a workforce of roughly 300, but their go-to-market focus is very different. Mollie thrives in the SME and e-commerce segment, while GoCardless has carved out a position in mid-market and enterprise recurring payments. Instead of trimming down, this offers an opportunity to design a segmented sales structure: Mollie’s teams focusing on small businesses, GoCardless on enterprise, and a new joint “strategic accounts” group built to target pan-European growth.

GoCardless also has a strength in customer success and operations, with established teams that are stable and longer-tenured. This is an underutilized asset that Mollie could lean on, particularly through GoCardless’ hub in Latvia. Expanding Mollie’s service footprint there while redeploying some of its back-office staff into customer-facing roles would both cut costs and improve service coverage.

2. Workforce planning – Aligning to the integration path

The integration model chosen will shape how the workforce evolves. A full integration would inevitably mean rationalizing overlapping functions such as HR, finance, and parts of sales. That might deliver short-term cost savings but would risk cultural shocks and morale issues, especially as Mollie’s and GoCardless’ work rhythms are so different. A stand-alone model would preserve the status quo, keeping teams intact and brands separate, but it would also leave duplication in place and miss out on potential synergies. Under hybrid integration model, back-end functions such as compliance, IT infrastructure, and risk could be merged to improve efficiency, while customer-facing roles, sales, support, product, remain intact in the short term. Workforce planning here must emphasize mobility and flexibility. Engineers could rotate between Mollie’s card stack and GoCardless’ open banking teams, while sales teams could learn to sell across both product sets. In this way, people aren’t just preserved, they’re actively developed into more versatile professionals.

3. Reskilling and redeployment opportunities

Reskilling will be central to making this acquisition work. Engineering teams should be retrained to bridge both sides of the payments spectrum, bank-to-bank infrastructure on one hand, and card/e-commerce systems on the other. This would enable the creation of cross-functional squads focused on developing a unified API platform.

Salespeople can be reskilled too. Mollie’s teams, used to pitching e-commerce solutions, could learn how to sell recurring and subscription models, while GoCardless’ enterprise sellers could be deployed into mid-market opportunities where Mollie has traction. Customer support provides another lever: GoCardless’ service teams, already strong in stability and experience, could take on more of Mollie’s volume from the Latvian hub. At the same time, both companies’ support staff could be upskilled into compliance and fraud monitoring roles, which are becoming increasingly critical in regulated payments markets.

Final recommended approach

The best approach is a phased hybrid integration. PayPal, for instance, kept Braintree and Venmo as separate brands. Stripe tends to integrate acquisitions into its platform but keeps the tech modular. For Mollie, this would likely mean keeping GoCardless as “a Mollie company” in the short term, while integrating back-end systems like compliance and infrastructure. Customer-facing functions would remain largely intact, at least initially. This path protects customer trust, preserves GoCardless’ brand value, and avoids the risks of a messy merger, while still delivering efficiency gains behind the scenes.

This acquisition should not be treated as a cost-cutting exercise. The numbers make it clear: the engineering bases are complementary, sales teams serve different markets, and GoCardless’ support hub is an underutilized strength that can be scaled.