Skip to content

Skip to content

Stablecoins are no longer just tools for crypto traders. Today, they handle billions in daily payments, support lending markets, and are slowly moving into mainstream finance. By mid-2025, their total market value is nearing $300 billion. USDT and USDC lead the way, but the real story is about the companies behind them.

These issuers are very different from each other. Some started in crypto’s early, messy days, others have roots in Wall Street, and a few come from Big Tech with a focus on scale and fast growth. Their hiring, internal setup, and partnerships show what they value most: trust, reach, or speed.

This piece looks at six of the most visible issuers, Circle, Tether.io, Paxos, Gemini, First Digital, and Stably. Together, they show how “digital money” is being designed, managed, and brought to market. Please note that all data is based on the first week of September, and figures may vary if reviewed at a later date.

Part 1: Employee Growth Velocity

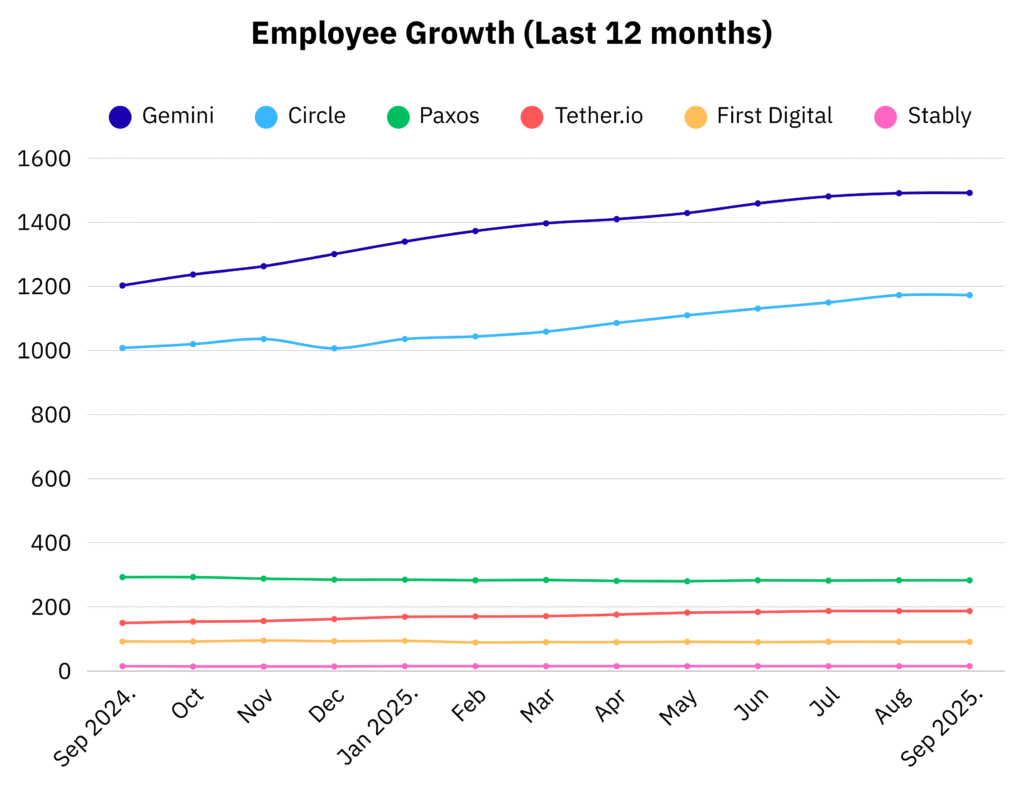

Over the past year, employee growth has clearly set the big issuers apart. Gemini leads with the strongest gains, growing nearly 25%, from 1,203 to 1,492 employees, showing steady month-by-month expansion. Circle comes next, adding about 165 people (from 1,008 to 1,173), showing steady but controlled growth.

Tether.io’s headcount rose more slowly, from 150 to 187, hinting at gradual hiring rather than a big expansion. Paxos stayed almost flat at around 280–293 staff, suggesting it’s focused on consolidation instead of growth. First Digital (around 89–95) and Stably (14–15) hardly moved at all, reflecting their small, stable place in the market.

In short, the numbers split issuers into three groups: fast growers (Gemini, Circle), slow movers (Tether.io), and those standing still (Paxos, First Digital, Stably).

Part 2: Who’s Doing the Heavy Lifting?

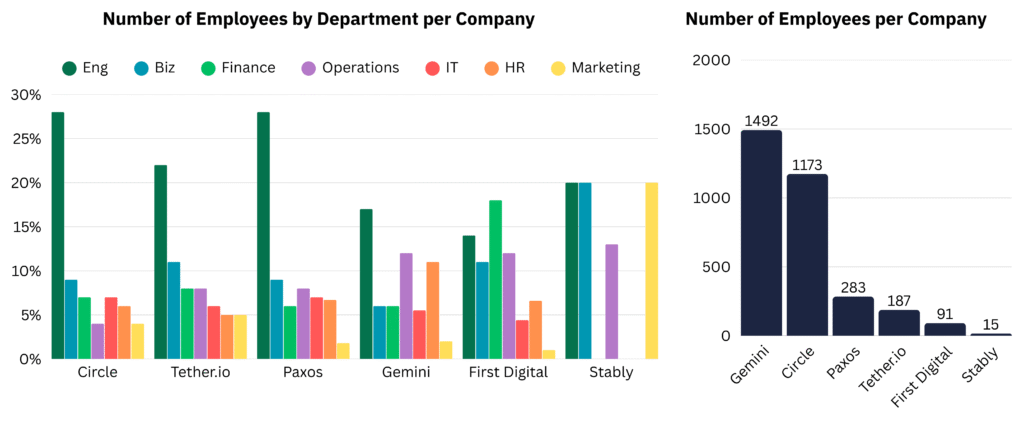

Headcount isn’t just a number. How companies staff up shows what they really care about.

Gemini (1,492) is the giant. But only 17% are engineers. HR (11%) and Ops (12%) take a bigger share, suggesting the exchange may lean more toward compliance and governance than pure tech, which fits with GUSD’s strong regulatory footing under NYDFS oversight and rules like 1:1 backing and monthly reserve reports.

Circle (1,173) looks more like a classic tech company: 28% engineers, backed by strong finance and IT teams. Product is at the center, supported by traditional financial discipline.

Tether.io (187) runs lean for the biggest stablecoin in the world. About 22% engineers keep its crypto core alive, while newer finance and ops hires hint at a move toward credibility.

Paxos (283) mirrors Circle’s engineering strength (28%) but maybe also backs that with one of the thickest compliance/regulation teams in the space. In fact, as part of its FIUSD deal with Fiserv, Paxos emphasizes “our proven, globally regulated stablecoin issuance and payments platform” as its selling point.

First Digital (91) leans heavily toward finance (18%). It feels less like a startup and more like a trust company that issues a stablecoin on the side.

Stably (15) is tiny, spreading its people across engineering, business development, and marketing (around 20% each). A classic startup setup: build fast, sell hard.

The bottom line: Circle and Paxos double down on engineering. Gemini and First Digital lean into compliance and operations. Tether.io stays small but tough. Stably looks more like a boutique shop with a product twist.

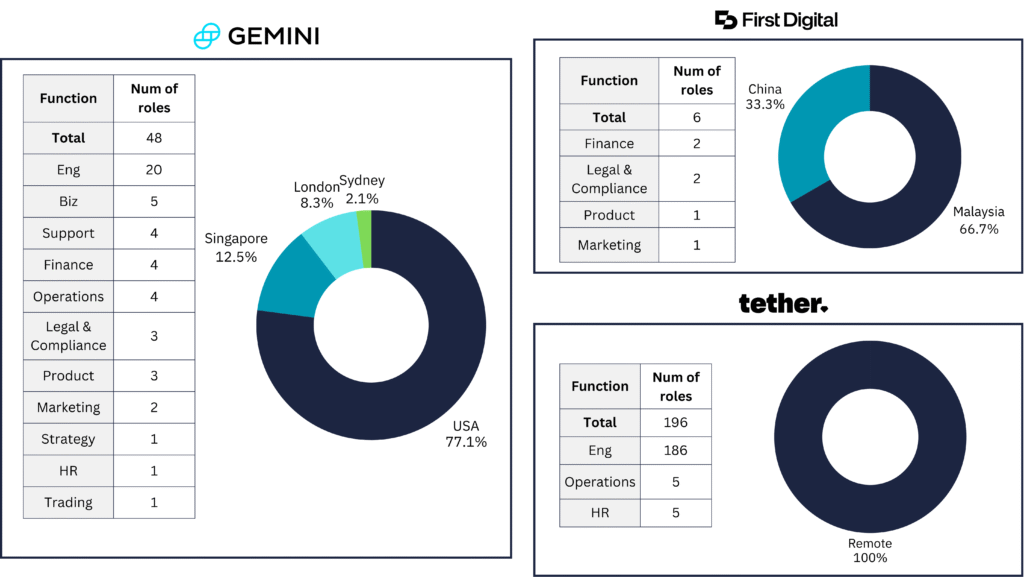

Part 3: Open Roles and Hiring Geography

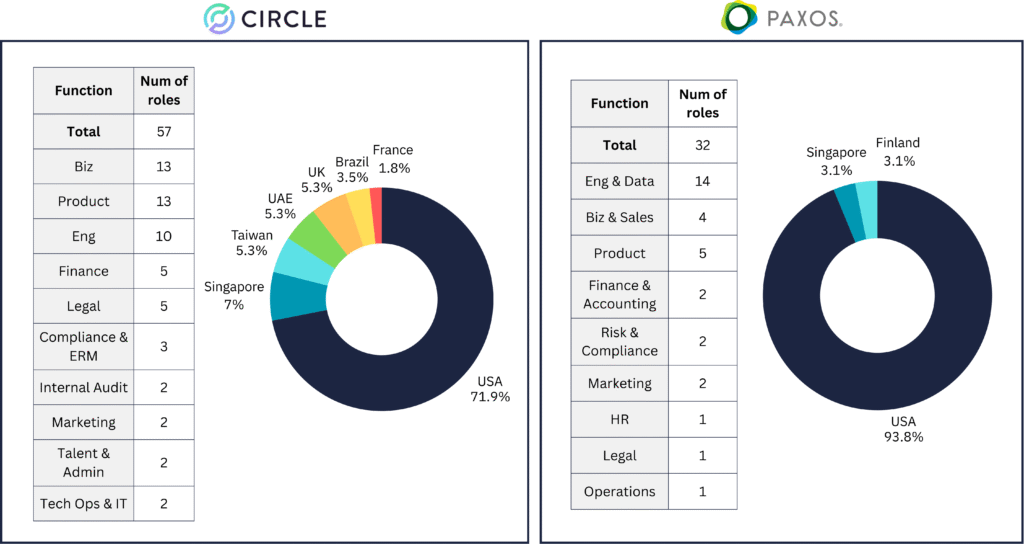

Circle

57 open roles worldwide, most in the U.S. (41). Smaller hubs in Singapore, Taiwan, UAE, UK, Brazil, and France.

- Hiring focus: Business (13) and Product (13) lead, followed by Engineering (10). Legal, compliance, audit, and finance together add 15 roles.

- Signal: Circle is pushing for institutional partnerships and global product growth. Engineering is steady, but most of the expansion is through Biz + Product to scale adoption worldwide.

Tether.io

196 open roles, almost all in Engineering (186). The rest: Ops (5) and HR (4).

- Geography: fully remote.

- Signal: Tether.io is doubling down on its crypto-native roots. No hubs, no compliance build-out, just a big push to expand engineering and ship products fast.

Paxos

32 open roles, mainly in Engineering & Data (14) and Product (5). Smaller numbers in Biz (4), Compliance/Legal (4), Finance (2), Ops (1), and Marketing (2).

- Geography: almost all U.S.-based (30), with just 1 each in Singapore and Finland.

- Signal: A classic enterprise infrastructure stance, focus at home, grow products, and strengthen regulatory credibility.

Gemini

48 open roles, with Engineering (20) leading. Others spread across Biz (5), Ops (4), Finance (4), Legal/Compliance (3), Product (3), and a few in support, marketing, HR, and trading.

- Geography: mostly U.S. (37), plus Singapore (6), London (4), Sydney (1).

- Signal: Balanced hiring, but with a tilt back to Engineering. Gemini is boosting technical capacity globally while keeping its regulatory backbone solid.

First Digital

6 open roles: Finance (2), Legal/Compliance (2), plus one in Product and one in Marketing.

- Geography: Malaysia (4) and China (2).

- Signal: True to its custody/compliance-first model. Growth is about trust and financial structure, not engineering, at least for now.

Stably

0 open roles.

- Signal: Staying lean. Growth here depends on projects, not headcount.

Part 4: Leadership DNA and Strategic Positioning

The backgrounds of senior leaders show what each issuer values most, crypto roots, financial discipline, or tech-driven growth. Paired with hiring choices, this defines how each is positioned in the market.

Circle: CEO Jeremy Allaire is a lifelong tech entrepreneur, with ColdFusion and Brightcove among his past ventures. His product chiefs (CPO, CTO) bring Big Tech experience from Google, Pinterest, and more, giving Circle strong technology DNA. At the same time, the CFO and Chief Compliance Officer come from investment banking and risk management. This mix, tech at the top, TradFi in finance and compliance, explains Circle’s role as a scaling fintech that blends innovation with regulatory trust.

Tether.io: CEO Paolo Ardoino is crypto through and through, having spent nearly his whole career at Tether.io and Bitfinex. Around him, though, the CFO and compliance lead come from hedge funds and global banks. Tether stays crypto at its core but has added financial veterans to boost credibility as it works with governments and institutions.

Paxos: CEO Charles Cascarilla is firmly TradFi, with roots in banking and asset management. But his team is a mix: a CTO and CFO from Big Tech and fintech, a CPO from Coinbase, and Chief Compliance Officer came from traditional finance. The blend, finance for institutions, tech for scale, crypto talent for credibility, fits Paxos’s identity as a regulated infrastructure provider for partners like PayPal and Mastercard.

Gemini: The Winklevoss twins give the firm crypto-native credibility as founders. Yet their CFO and Chief Compliance Officer hail from Goldman Sachs, Morgan Stanley, and top AML roles. This leaves Gemini straddling two identities: crypto-native leadership on the surface, but a culture of compliance and governance reinforced by its New York trust charter.

First Digital: CEO Vincent Chok built his career in trusts, private wealth, and capital markets before moving into crypto custody. The CFO is an auditor and finance veteran, while the CPO has a banking background at HSBC and Nordea. Nearly the whole team is TradFi talent entering crypto custody, which explains why First Digital positions itself as a trusted custodian in Asia rather than a crypto-native disruptor.

Stably: CEO Kory Hoang started at Bank of America and Merrill Lynch before pivoting to crypto, while CTO David Zhang brings Big Tech credentials from Amazon. The mix, finance roots, crypto leadership, and tech product strength, gives Stably a hybrid profile. But with a small, founder-led team, it runs more like a nimble startup than a major issuer.

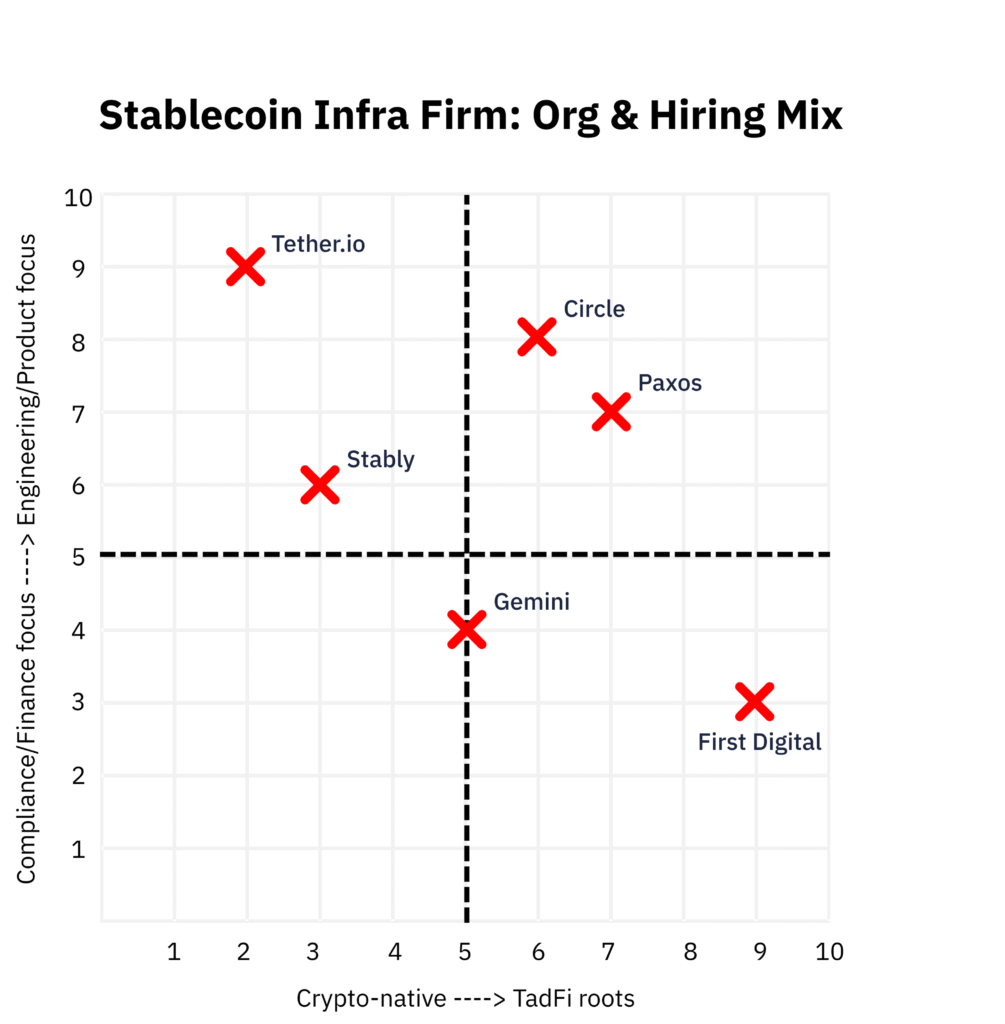

Part 5: Mapping the Landscape

When leadership DNA is combined with organisational structures and hiring signals, the differences sharpen. Using the axes of Crypto-native ↔ TradFi roots (X-axis) and Compliance-heavy ↔ Engineering/Product-heavy (Y-axis), the issuers’ position is as follows:

- Circle: A tech-driven fintech with strong institutional polish.

- Tether.io: Deeply crypto-native, engineering-first, layering in TradFi credibility.

- Paxos: Regulated TradFi roots, balanced with tech and crypto-native leadership.

- Gemini: Split between crypto-native founders and TradFi execs, but culture tilted toward compliance.

- First Digital: Strongly TradFi, finance/compliance heavy, small engineering footprint.

- Stably: Startup with crypto-native leadership and Big Tech product DNA, lean and infra-focused.

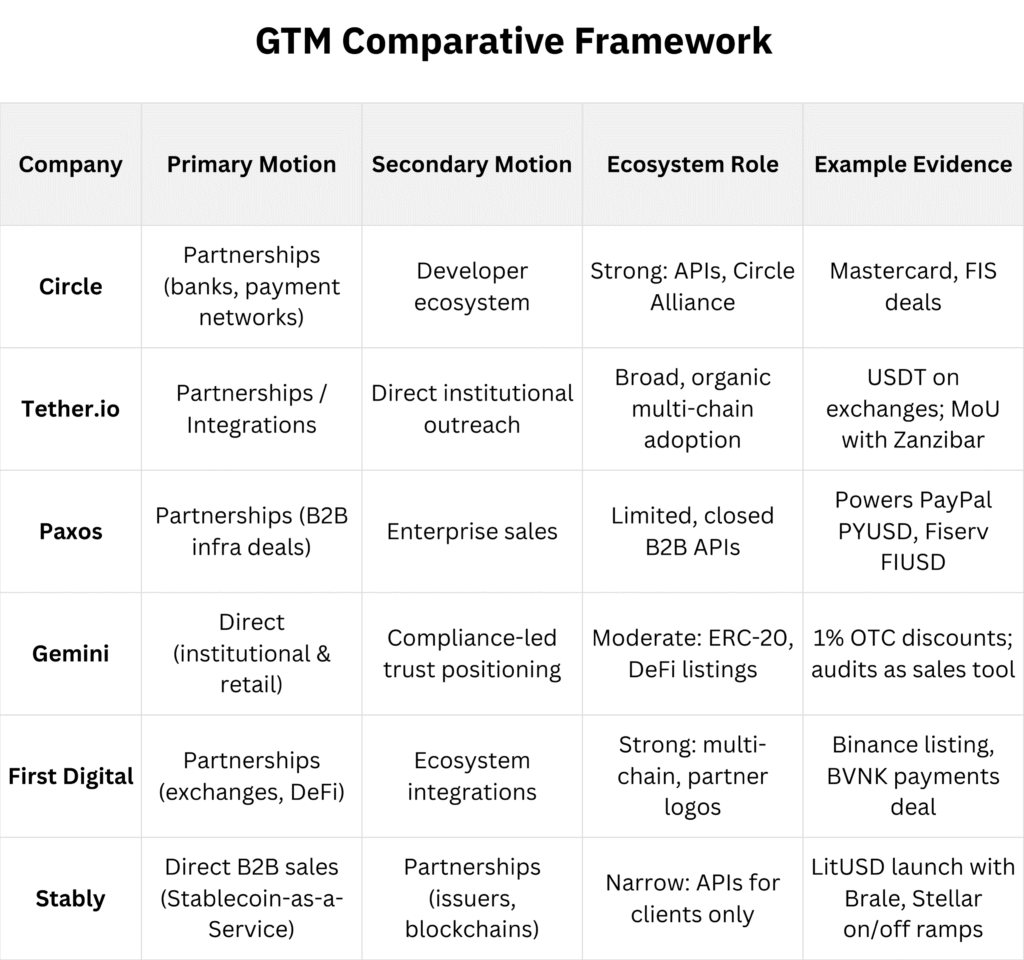

Part 6: How Stablecoin Issuers Go to Market: Partnerships, Direct Sales, and Ecosystem Plays

Stablecoins aren’t just tokens, they’re products that need distribution. Behind each issuer is a go-to-market strategy that drives adoption. Some lean on heavyweight partnerships, others push direct enterprise sales, and a few bet on open ecosystems where developers do the scaling. Looking at Circle, Tether.io, Paxos, Gemini, First Digital, and Stably, the differences stand out.

Circle (USDC) runs a two-track play: big partnerships and a developer ecosystem. Deals with Mastercard and FIS plug USDC into payment rails, while the Alliance Program and APIs bring in startups and fintechs to build use cases. Circle isn’t chasing sales desks, it’s betting on network effects. Partners give it reach, developers add stickiness, and USDC becomes the bridge between TradFi and Web3.

Tether.io (USDT) won by ubiquity: listed on nearly every exchange, running on multiple blockchains, and deeply woven into DeFi. That reach is its moat. But recently, Tether has shifted, launching campaigns in Brazil, signing MoUs with governments like Zanzibar, and holding talks with U.S. banks. Still crypto-native at heart, but now layering in enterprise sales to court institutions.

Paxos takes a different tack. It doesn’t push its own brand; instead, it powers others: PayPal’s PYUSD, Fiserv’s FIUSD, even Binance’s BUSD in the past. Its playbook is pure B2B infrastructure, compliance as the hook, enterprise sales as the driver. Paxos sells reliability to big institutions, who then scale the product to millions. Unlike Circle, it doesn’t run an open developer ecosystem.

Gemini (GUSD) has always favored direct distribution. Back in 2018, it gave OTC desks discounts to spark liquidity. Today, its pitch is “safety first”, audited, regulated, cautious. GUSD sits on DeFi as ERC-20, but integrations are mostly standard listings, not deep partnerships. Gemini leans on its exchange and regulatory trust, which keeps GUSD steady but smaller than Circle or Paxos.

First Digital (FDUSD) launched in 2023 with a Binance listing that instantly propelled it into the big leagues. From there, it went all-in on partnerships, splashing its name across exchanges, blockchains, liquidity providers, and DeFi protocols. Its model: get listed everywhere, integrate widely, and let usage snowball. Fast scale, without a heavy sales push.

Stably takes a different route altogether. It doesn’t chase mass adoption of one token. Instead, it sells “Stablecoin-as-a-Service,” building custom coins for banks, fintechs, and brands. That makes its GTM pure enterprise sales, pitching clients, walking them through compliance, and stitching together custodians and networks. Deals like LitFinancial’s litUSD and partnerships with Stellar and Brale show how Stably works: part consultancy, part infrastructure provider.

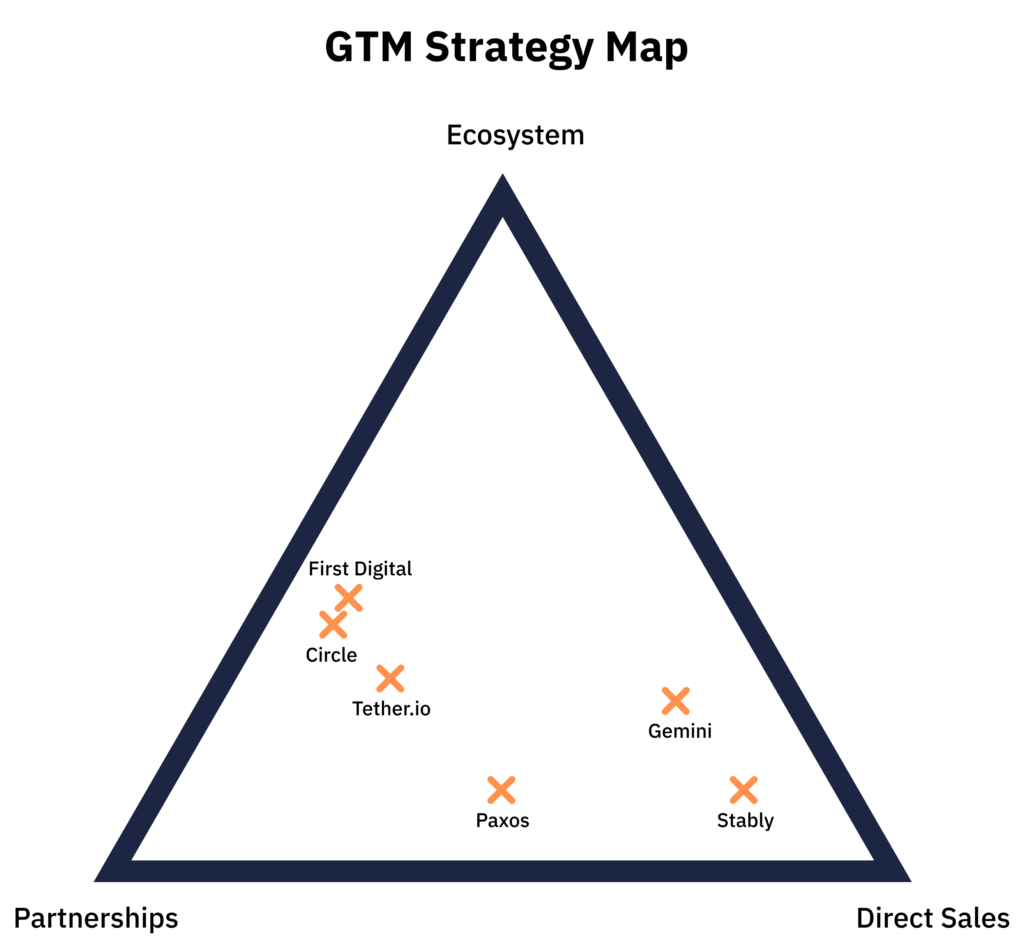

Part 7: The Strategy Map

On the Partnerships ↔ Direct Sales ↔ Ecosystem spectrum, here’s where they land:

- Circle & First Digital → partnership-heavy with strong ecosystems.

- Tether.io → partnership/everywhere coin, now inching toward direct institutional sales.

- Paxos → partnership + enterprise sales, powering others’ coins.

- Gemini → mostly direct, with compliance and trust as the hook.

- Stably → pure direct sales model, closer to SaaS than a classic issuer.

In other words: Circle, Tether.io, and First Digital build ecosystems; Paxos and Gemini mix partnerships with direct sales; Stably sells infrastructure one client at a time.

Conclusion: The Battle Lines of Stablecoin Issuers

The comparison across Circle, Tether.io, Paxos, Gemini, First Digital, and Stably shows how differently each issuer is positioning itself. Some are expanding through global partnerships and ecosystems, others are leaning on direct enterprise sales, while a few remain closer to their crypto-native roots. Their executive hires, open roles, and geographic footprints all signal priorities: whether it is engineering scale, compliance leadership, or business development.

What becomes clear is that stablecoin competition is not only a matter of technology or regulation, but also of people. The balance between crypto-native expertise, traditional finance experience, and big tech scaling skills will determine which models succeed.

At PCN, we follow these shifts closely because they directly impact hiring needs. As issuers refine their strategies, the ability to identify and recruit the right talent, from compliance executives to engineering leaders and commercial specialists, becomes a decisive factor. Building the right teams is ultimately what allows these strategies to move from intent to execution.